A stablecoin is, at its core, a promise.

Not a complicated promise. Not a promise backed by gold reserves, or sovereign guarantees, or centuries of institutional credibility. A promise that one digital token is worth one dollar, because the issuer says so, and because enough people have agreed to believe it simultaneously that the agreement itself has become a kind of infrastructure. This is, when you examine it carefully, either a remarkable feat of collective financial engineering or an extraordinarily elegant confidence trick. Possibly both. The $300 billion currently sitting in stablecoins suggests that, for now, the market has declined to make the distinction.

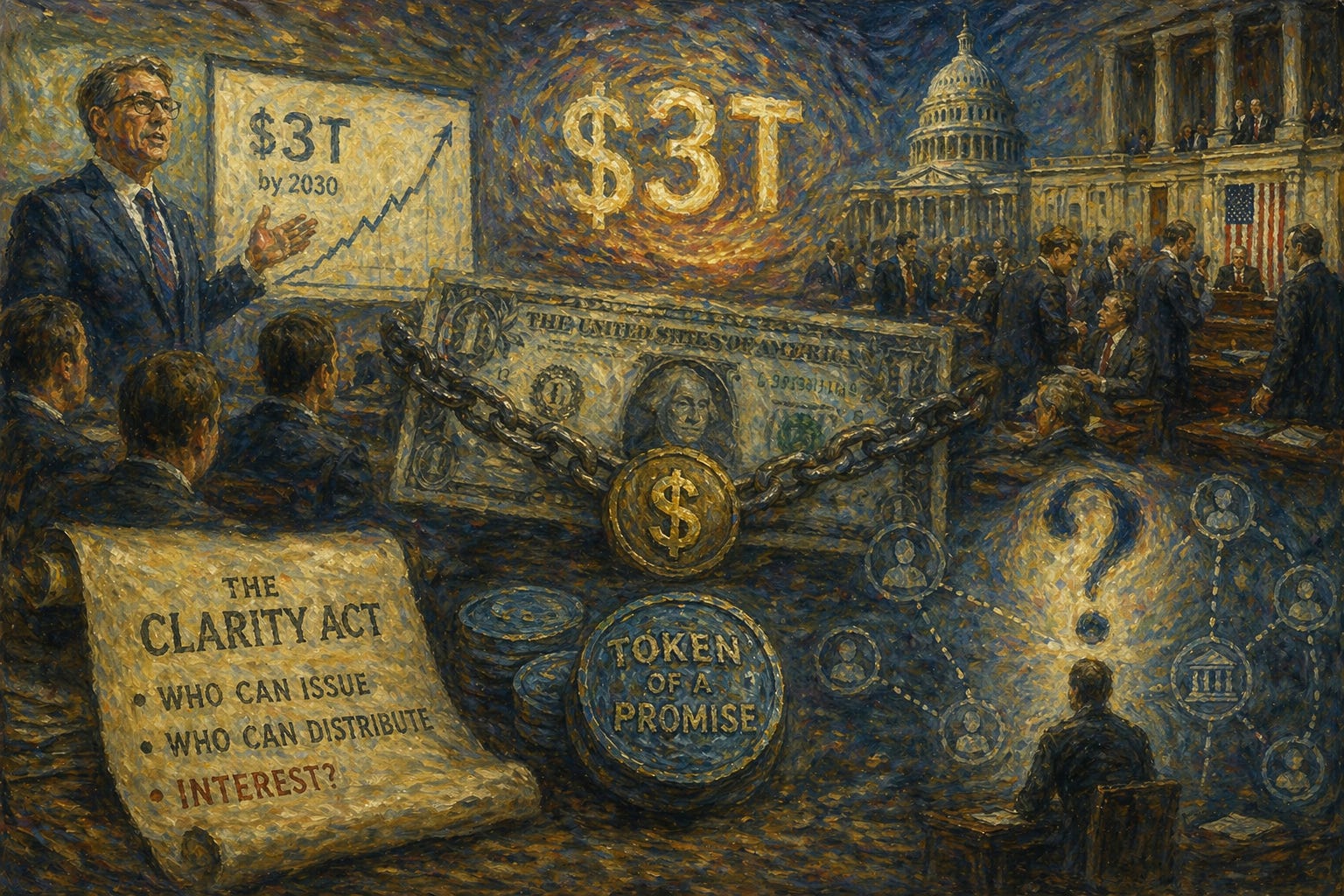

Treasury Secretary Scott Bessent projects that this market will reach $3 trillion by 2030. Three trillion dollars. Denominated in a currency that is itself a promise, held in tokens that are a promise about the promise, governed by a regulatory framework that the United States Senate is still, at time of writing, attempting to agree on. The Clarity Act, currently under debate, is designed to establish who can issue stablecoins, who can distribute them, and the part that has caused the most excitement, whether the holders of these digital dollar promises should be allowed to earn interest on them.

This last question has reduced the American banking lobby to what can only be described as a state of institutional distress.

The banks’ position is straightforward. If stablecoins pay yield, depositors will move money out of bank accounts and into stablecoins. Banks will have fewer deposits. Fewer deposits mean less lending. Less lending means less credit to the real economy. The stablecoin, in this framing, is an existential threat to the deposit franchise that underpins the entire American credit system. The banks would like you to know they are very concerned. They would like the Senate to share that concern. They would prefer, if at all possible, that Congress resolve it by ensuring stablecoins cannot compete with them on yield.

The Council of Economic Advisers (CEA) has weighed in with a paper estimating that a yield prohibition on stablecoins would raise aggregate bank lending by approximately $2.1 billion, 0.02 per cent of outstanding loans. Two point one billion dollars. In a $23 trillion economy. The banks, one might observe, are experiencing existential dread about a rounding error.

The CEA’s argument rests on what it calls deposit recycling. When a depositor withdraws cash from Bank A to buy a stablecoin, the stablecoin issuer uses that cash to purchase Treasury bills. The dealer who sells those Treasury bills redeposits the proceeds into the banking system. Net result: deposits shuffle around the system rather than leaving it. The banks’ fears, on this account, are overblown.

This argument has the pleasing elegance of a mechanism that works perfectly in theory and approximately never in practice. As any bank risk officer will tell you, the assumption that a stablecoin-driven outflow at scale produces a clean recycling loop requires every participant in the chain to behave exactly as modelled, in sequence, without introducing any friction, delay, or alternative use of the proceeds. When a bank faces a large liability outflow, it does not sit passively. It adjusts assets. The likely adjustment is to shed liquid securities. Treasury bonds, for instance. The dealer who buys those bonds may well use the cash from a T-bill sale to acquire them, at which point no net redeposit occurs and the recycling loop does not close. The CEA’s model is not wrong, exactly. It is the kind of correct that dissolves on contact with the real world.

But here is the thing the banks do not want said too loudly: the threat to their deposit franchise from stablecoins is, at present, largely theoretical.

Yield-conscious depositors have had alternatives to bank accounts since the 1970s. Money market funds which pay market-rate returns on cash holdings and are regulated, liquid, and operated by some of the most established names in asset management have grown to $7.5 trillion in the United States. Checking account balances sit at $7.8 trillion. The two figures have existed in rough parity for decades. Despite fifty years of competition from money market funds, US commercial bank deposits stand at approximately $18 trillion. The deposit franchise has not been destroyed by yield competition. It has coexisted with it.

Why? Because most people do not hold their current account balance primarily for yield. They hold it because their salary lands there, their direct debits leave from there, their debit card is connected to it, and switching requires an afternoon of administrative inconvenience they cannot be bothered with. The bundling of transactional convenience with deposit-holding is what protects bank deposits, not the absence of better-yielding alternatives. Yield alone, as five decades of money market fund history demonstrates, is insufficient to capture transactional balances at scale.

For stablecoins to pose a genuine threat to the deposit franchise, they would need to become conveniently spendable at the point of sale — integrated into payroll systems, card networks, and the everyday transactional infrastructure that currently anchors deposits in bank accounts. They are not there yet. This is not a regulatory opinion. It is an observation about where you can currently pay for your Pret a Manger with a stablecoin. The answer is nowhere.

The more honest framing of the stablecoin yield debate, then, is not whether it threatens American banking. The more honest framing is what it reveals about who is actually threatened, and why, and whether the regulatory response reflects a genuine analysis of systemic risk or a successful lobbying campaign by incumbents using the language of systemic risk.

The banks are worried. That is true. But the banks are worried in the way that established industries are always worried when a new instrument begins to accumulate assets and build distribution. They are worried about competition. They are expressing this worry in the language of macro-prudential concern. Credit supply, deposit stability, systemic fragility. That is the language that moves legislatures. The translation from competitive anxiety to macro-prudential framing is a well-practised art. The tobacco industry was worried about public health regulation. The taxi industry was worried about passenger safety. The banks are worried about the deposit franchise.

These worries are not entirely dishonest. The systemic implications of a $3 trillion stablecoin market are genuinely unclear. A run on a major stablecoin issuer could transmit stress through the Treasury bill market in ways that are not fully modelled. The history of instruments that promised stable value and delivered periodic catastrophe is not short. The Reserve Primary Fund broke the buck in 2008 on the back of Lehman exposure. Various algorithmic stablecoins have collapsed entirely. TerraUSD, a stablecoin that was not backed by dollar reserves at all but by a companion token and the collective willingness of its holders to believe, evaporated $40 billion in value over approximately 72 hours in May 2022. The promise, in that case, was worth precisely what it cost to make.

This is the central absurdity that the Senate’s deliberations, the CEA’s deposit-recycling models, and the banking lobby’s macroprudential anxiety all share a tendency to dance around: the $300 billion currently in stablecoins, projected to become $3 trillion, is denominated in a currency whose own stability rests on the credibility of the Federal Reserve, the Treasury, and the full faith and credit of the United States government. All of which are, in the final analysis, also promises. The dollar is a stablecoin. It is pegged to itself. It is worth a dollar because the United States government says it is, and because enough people have agreed to believe it simultaneously that the agreement has become civilisational infrastructure.

The difference, and it is an important difference, is that the dollar’s promise is backed by the world’s largest military, the deepest bond market in human history, and two and a half centuries of institutional development. The promise behind Tether, the largest stablecoin by market capitalisation, is backed by an audit that the company spent several years declining to provide and a reserve composition that analysts have described, with characteristic understatement, as opaque. These are not equivalent promises. The regulatory framework that treats them as analogous instruments requiring equivalent yield rules is, to put it mildly, doing a lot of work.

The Clarity Act’s genuine contribution, if it passes in a sensible form, would be to establish reserve requirements and transparency obligations that make the stablecoin promise more legible. A stablecoin issuer required to hold short-duration Treasuries or central bank reserves in full against outstanding tokens, subject to regular independent audit, is materially different from an issuer operating under self-reported reserve adequacy. The yield question matters. The reserve question matters more.

What is most interesting about the stablecoin debate, from an investment perspective, is not the domestic banking threat but the international one. Bessent’s $3 trillion projection is only plausible if a significant portion of that growth comes from outside the United States. And outside the United States, in the emerging markets where currencies are volatile, inflation is structural, and access to dollar accounts is restricted or unavailable, stablecoins are already functioning as a genuine financial service rather than a fintech novelty. A person in Lagos or Caracas holding dollar stablecoins on their phone is not making a speculative investment. They are protecting their savings from currency debasement using the most accessible instrument available. That is a real use case. It is growing. It will not be constrained by whatever the Senate decides about yield caps on American exchanges.

The $3 trillion, if it arrives, will be built largely on that demand. And the American banking lobby’s concern about deposit competition will look, in retrospect, rather like the CEA’s recycling model: technically interesting, practically marginal, and comprehensively beside the point.

There is a promise at the centre of all of this. Several promises, in fact, nested inside each other like financial matryoshka dolls. The stablecoin promises to be worth a dollar. The dollar promises to hold its value. The Senate promises to write a law that clarifies everything. The banks promise that their concerns are systemic rather than competitive.

Some of these promises will be kept. The question, as always with promises, is which ones and what happens to the $3 trillion when the answer becomes clear.