In the annals of financial history, few phrases have proved as prescient as those penned by Jeremy Warner in his article — The stock market is a timebomb waiting to go off. There is a a giant, all-consuming investment bubble at the heart of the global economy — published in The Telegraph on 27 Sep 2025 regarding the cyclical nature of market excess. From AOL’s catastrophic marriage to Time Warner, through RBS’s suicidal pursuit of ABN AMRO, to Nvidia’s extraordinary $100 billion commitment to OpenAI, each era produces its own spectacular monument to hubris. What makes these episodes particularly fascinating—and maddening—is not their inevitability, but rather our collective ability to spot the warning signs whilst remaining utterly powerless to heed them.

The observation that “everyone can see these warning signs, and yet it makes no difference” strikes at the heart of financial market psychology. We find ourselves witnessing, once again, the peculiar phenomenon where rational analysis collides with irrational exuberance, where sober warnings are drowned out by the intoxicating melody of easy profits, and where the phrase “this time is different” becomes the mantra of a generation about to learn, once more, that it never is.

The Case for Inevitability: Why Bubbles Are Features, Not Bugs

The Dotcom Precedent: AOL and the Theatre of Digital Delusion

The AOL-Time Warner merger stands as perhaps the most spectacular example of bubble-era thinking translated into corporate action. In January 2000, at the height of dotcom mania, this $182 billion union promised to marry the digital future with traditional media assets. The vision was seductive: AOL’s 30 million subscribers would provide instant distribution for Time Warner’s content, whilst Time Warner’s vast media empire would give substance to AOL’s inflated valuation.

Yet the warning signs were blindingly obvious to anyone willing to see them. AOL’s business model depended entirely on dial-up internet subscriptions in an era when broadband was already emerging. The company’s revenue growth was increasingly dependent on accounting gymnastics and unsustainable advertising spending from other dotcom companies. Most tellingly, AOL’s market capitalisation exceeded that of established media giants despite having a fraction of their assets or revenue streams.

The merger’s architects, led by AOL’s Steve Case and Time Warner’s Gerald Levin, dismissed such concerns with the era’s characteristic hubris. They spoke of “synergies” that would transform both companies, of a “new paradigm” where traditional valuation metrics no longer applied. The deal was structured to favour AOL shareholders, giving them 55% control of the combined entity despite Time Warner’s superior asset base—a clear indication that market euphoria had completely divorced stock prices from underlying value.

When the dotcom bubble burst just months after the merger’s completion, the folly became apparent with brutal clarity. The combined company posted a staggering $99 billion loss in 2002, then the largest in corporate history. By 2009, Time Warner had spun off AOL entirely, essentially admitting that the most expensive merger in history had created no value whatsoever. The episode perfectly encapsulated bubble psychology: rational people making irrational decisions because the collective delusion made such decisions appear not just sensible, but inevitable.

The Banking Sector’s Suicide Note: RBS and ABN AMRO

If the AOL-Time Warner merger demonstrated how technology euphoria could cloud judgment, the RBS-ABN AMRO takeover revealed how competitive dynamics during bubble periods can drive even sophisticated institutions toward self-destruction. In May 2007, as credit markets were already showing signs of strain, RBS led a consortium that paid €71.1 billion for ABN AMRO—a price that would prove catastrophic when the financial crisis erupted just months later.

The warning signs were even more glaring than in the dotcom era. Sir Fred Goodwin, RBS’s chief executive, was explicitly warned by advisers about ABN AMRO’s exposure to toxic assets, particularly collateralised debt obligations (CDOs) that would prove nearly worthless. UBS banker John Cryan, who advised RBS, told Goodwin he was “extremely concerned” about the impact on RBS’s capital ratios, warning that ABN AMRO contained “stuff we can’t even value”. Goodwin’s response—“Stop being such a bean counter”—perfectly captured the bubble mentality where caution was dismissed as timidity.

The acquisition doubled the size of RBS’s trading book to £470 billion, supported by just £2.3 billion in capital. This leverage ratio of over 200:1 would have been considered suicidal in normal times, yet during the credit bubble, it seemed merely aggressive. The fact that RBS could only conduct “extremely limited due diligence” on ABN AMRO should have been disqualifying, yet the competitive dynamics of the bubble made such recklessness appear prudent.

The aftermath was swift and devastating. RBS posted a £24 billion loss—then the largest in UK corporate history—with £16 billion attributed directly to the ABN AMRO acquisition. The bank required a £46 billion taxpayer bailout and remains partially government-owned to this day. The episode demonstrated how bubble psychology doesn’t just affect individual investors but can capture entire institutions, leading sophisticated financial professionals to make decisions they would never contemplate under normal circumstances.

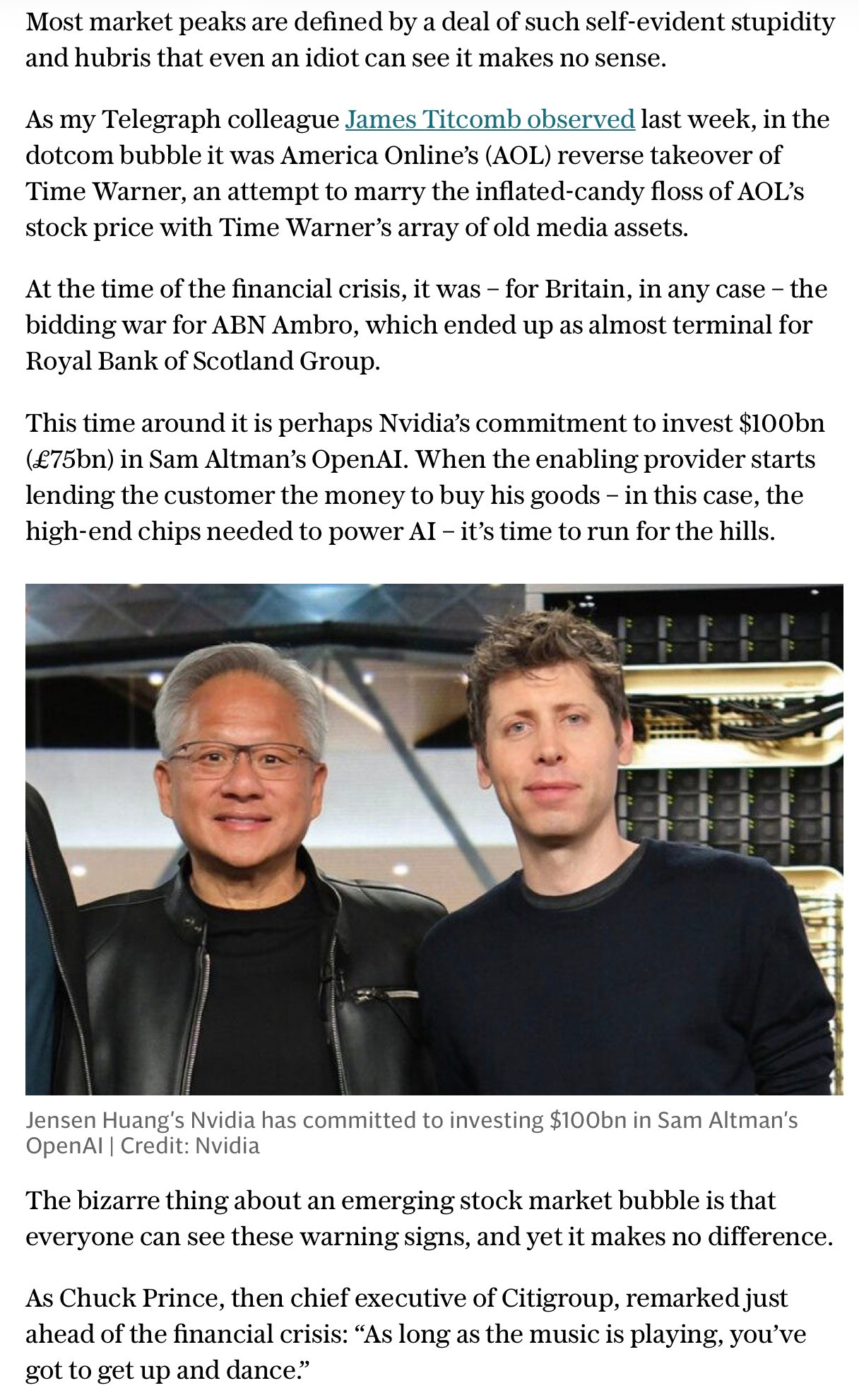

The AI Renaissance: Nvidia’s $100 Billion Circular Logic

Today’s AI bubble exhibits all the classic warning signs that preceded previous crashes, yet with a modern twist that makes the circular financing even more explicit. Nvidia’s commitment to invest $100 billion in OpenAI, which will then use those funds to purchase Nvidia’s chips, represents vendor financing taken to an almost absurd extreme. The arrangement is so transparently circular that analysts openly describe it as “bubble-like behaviour”, yet it proceeds regardless.

The parallels to previous bubbles are striking. Like the dotcom era, we have a transformative technology—artificial intelligence—that promises to revolutionise everything from healthcare to transportation. Like the credit bubble, we have massive capital deployment based on projections rather than proven returns. And like all bubbles, we have the familiar refrain that “this time is different” because AI represents a fundamental shift in human capability.

The circular financing aspect is particularly reminiscent of the late 1990s, when telecommunications equipment manufacturers like Cisco and Nortel provided loans and credit to customers who then used those funds to purchase equipment. Wall Street research firm NewStreet Research estimates that for every $10 billion Nvidia invests in OpenAI, it will generate $35 billion in GPU sales—a return that would represent 27% of Nvidia’s annual revenue. Such arrangements create artificial demand that can sustain inflated valuations far longer than market fundamentals would suggest.

Yet the warning signs are everywhere. Nvidia’s investment portfolio has exploded from 41 deals in 2024 to 51 in just the first three quarters of 2025. The company’s publicly traded holdings have grown to $4.33 billion, whilst its non-marketable equity investments have increased to $5.8 billion Most tellingly, the vast majority of these investments are in companies that either use Nvidia’s chips or develop complementary technologies—creating a web of interdependent relationships that amplifies both upside and downside risks.

The Case for Scepticism: Why This Time Truly Isn’t Different

The Psychology of Perpetual Delusion

The most compelling argument against bubble mentality lies not in economics but in psychology. Sir John Templeton’s famous observation that “the four most dangerous words in investing are ‘this time it’s different’” captures a fundamental truth about human nature: our tendency to believe that current circumstances exempt us from historical patterns. This cognitive bias explains why intelligent people repeatedly make the same mistakes across different asset classes and time periods.

The psychological mechanisms driving bubble behaviour are remarkably consistent across centuries. Whether we examine Dutch tulip mania in the 1630s, the South Sea Bubble of 1720, or the dotcom crash of 2000, the patterns remain identical. Initial innovation or opportunity attracts early investors, generating genuine returns that create positive feedback loops. Media coverage amplifies success stories, whilst FOMO (fear of missing out) draws in progressively less sophisticated participants. Confirmation bias ensures that investors seek information supporting their positions whilst ignoring contradictory evidence.

The herding behaviour described by Charles Kindleberger becomes particularly pronounced during the euphoria phase, when “firms or households see others making profits from speculative purchases and resales” and “tend to follow”. This democratisation of speculation brings in “segments of the population that are normally aloof from such ventures,” creating the conditions for maximum damage when reality inevitably reasserts itself.

What makes current conditions particularly dangerous is the speed at which information travels and the interconnectedness of global markets. Social media amplifies both positive and negative sentiment, whilst algorithmic trading can accelerate price movements beyond human comprehension. The result is bubble formation that occurs faster but with greater intensity than historical precedents.

The Circular Financing Red Flag

Perhaps the most damning evidence against current market conditions lies in the prevalence of circular financing arrangements that characterised previous bubble peaks. When vendors begin lending money to customers to purchase their own products, it suggests that genuine demand has been exhausted and artificial demand must be created to sustain growth trajectories.

The telecommunications bubble of the late 1990s provides the clearest historical parallel. Companies like Cisco, Lucent, and Nortel provided financing to customers who then used those funds to purchase networking equipment. This created the illusion of robust demand whilst actually representing vendor-financed inventory accumulation. When the bubble burst, these arrangements unwound catastrophically as customers defaulted on loans and returned equipment they could no longer afford.

Nvidia’s arrangements with OpenAI and other AI companies exhibit precisely the same characteristics. The company’s statement that its investment “would not be used for any direct purchases of Nvidia products” appears disingenuous when OpenAI has explicitly stated it will use the funding to purchase millions of Nvidia chips. The fact that such arrangements require elaborate disclaimers suggests their architects understand the problematic optics, yet proceed regardless.

The scale of circular financing in the AI sector extends far beyond Nvidia. Meta is negotiating a $20 billion cloud computing deal with Oracle, whilst Microsoft pursues similar arrangements. The fact that Microsoft, Meta, Amazon, Alphabet, and Tesla collectively account for over 40% of Nvidia’s revenue creates a web of interdependence that amplifies systemic risk. When the inevitable correction occurs, these circular arrangements will collapse simultaneously, creating cascading effects throughout the technology sector.

The Valuation Disconnect

Traditional valuation metrics suggest that current market conditions have reached or exceeded previous bubble peaks. The S&P 500 is trading in the top 10% of historical valuations relative to earnings, whilst AI-related stocks exhibit price-to-earnings ratios that would have been considered absurd during calmer periods. Yet these metrics are increasingly dismissed by investors who argue that AI represents such a fundamental shift that historical comparisons are irrelevant.

This dismissal of traditional valuation methods precisely mirrors the rhetoric of previous bubbles. During the dotcom era, investors abandoned price-to-earnings ratios in favour of “price-to-clicks” and other novel metrics that justified increasingly extreme valuations. The housing bubble saw similar innovations, with debt-to-income ratios dismissed as outdated measures that failed to capture new financing innovations.

The current AI bubble has produced its own valuation innovations, with investors focusing on potential rather than actual revenue, on total addressable markets rather than current market share, and on theoretical capabilities rather than demonstrated profitability. OpenAI’s $157 billion valuation, despite losing money on every customer interaction, perfectly encapsulates this disconnect between price and value.

Most concerning is the apparent acceptance of these valuations by sophisticated institutional investors who should know better. The fact that pension funds, sovereign wealth funds, and endowments are participating in these rounds suggests that bubble psychology has captured not just retail investors but the entire institutional investment community.

The Inevitable Conclusion: History’s Stubborn Refusal to Learn

Why We Never Learn

The most depressing aspect of financial bubbles lies not in their occurrence—which is inevitable—but in our collective inability to learn from previous episodes. Each generation convinces itself that its circumstances are unique, that its technology is truly transformative, and that historical patterns no longer apply. This cognitive arrogance ensures that bubbles will continue to form with predictable regularity, each one bringing fresh victims who believed they had unlocked the secret to perpetual wealth creation.

The human brain’s tendency toward optimism bias plays a crucial role in this process. We systematically underestimate the likelihood of negative outcomes whilst overestimating our ability to time markets and exit before crashes occur. This bias becomes particularly pronounced during bubble periods, when recent positive returns create false confidence in our predictive abilities.

Financial memory, as observers note, extends just twenty years—precisely the time required for a new generation of investors to enter markets without direct experience of previous crashes. This ensures that hard-learned lessons are forgotten, allowing the same mistakes to be repeated with fresh enthusiasm. The investors who lived through the dotcom crash are now approaching retirement, whilst those driving current AI valuations have no memory of what happens when reality collides with speculation.

The Regulatory Capture Problem

Government and regulatory responses to bubbles typically arrive too late to prevent damage and often exacerbate problems through well-intentioned but misguided interventions. The Sarbanes-Oxley Act, passed in response to dotcom-era accounting scandals, imposed costs on public companies without preventing the subsequent housing bubble. The Dodd-Frank Act, designed to prevent another financial crisis, failed to address the leverage and speculation that characterised the pre-2008 period.

Current regulatory approaches to AI appear similarly inadequate to address bubble risks. Policymakers focus on hypothetical future risks from artificial general intelligence whilst ignoring present dangers from speculative excess and circular financing. This misallocation of regulatory attention ensures that bubbles can develop unchecked until they reach crisis proportions.

The problem is compounded by regulatory capture, where the industries being regulated effectively control their regulators through revolving door employment and political contributions. The same officials who should be warning about AI bubble risks are often former employees of the companies creating those risks, ensuring that warnings are muted and interventions delayed until after maximum damage has occurred.

The Eternal Return

The tragic irony of financial bubbles lies in their perfect predictability coupled with our complete inability to prevent them. We can identify the warning signs with scientific precision: circular financing, valuation extremes, psychological euphoria, and the inevitable dismissal of historical precedent. Yet this knowledge proves useless because bubbles are not rational phenomena but psychological ones, driven by emotions and incentives that remain impervious to logical argument.

The current AI bubble will end like all its predecessors: with sudden recognition that the emperor has no clothes, followed by panic selling, corporate bankruptcies, and shocked bewilderment at how obviously unsustainable arrangements were allowed to persist for so long. Nvidia’s circular financing with OpenAI will be dissected in business schools as a case study in bubble-era excess, just as AOL-Time Warner and RBS-ABN AMRO are studied today.

Yet even as I write these words, new bubbles are forming in sectors we cannot yet imagine, driven by technologies that seem genuinely transformative and populated by investors convinced that this time truly is different. The cycle continues not because we lack knowledge but because knowledge is powerless against the fundamental human emotions of greed, fear, and the eternal hope that we can somehow escape the gravitational pull of financial gravity.

Perhaps that is the ultimate lesson of financial bubbles: not that we should learn to prevent them, but that we should learn to expect them, prepare for them, and remember that in the grand casino of financial markets, the house always wins in the end. The only question is whether we will be among the early winners who exit before the music stops, or among the inevitable losers who discover too late that the chairs have all been taken away.

The Telegraph’s observation about everyone seeing the warning signs yet continuing regardless captures the essential tragedy of human financial behaviour. We are doomed to repeat history not because we don’t know better, but because knowing better has never been enough to overcome the intoxicating allure of easy money and the eternal belief that we, unlike all who came before us, have finally cracked the code to perpetual prosperity.

In the end, perhaps the most honest response to bubble warning signs is not to congratulate ourselves on our superior insight, but to acknowledge our own susceptibility to the same psychological forces that have driven financial excess for centuries. The bubble will burst—that much is certain. The only uncertainty is when, and whether we will be wise enough to step aside before it does.