The Everything Exchange - Coinbase Q3 2025

Is my investment thesis reaffirmed? Let's check if Brian and team are executing on their vision.

“With regulatory clarity accelerating, crypto rails are set to power more and more of global GDP for trading, payments in every financial service. Coinbase is well positioned to be the partner of choice for companies and financial institutions including Citi, which we just announced last week, who are looking to come onchain.” - Coinbase CEO Brian Armstrong, Q3-2025 Earnings Call.

This quarterly update covers Coinbase (COIN 0.00%↑ ). One of the most essential companies that global finance and governments can no longer ignore. That means no matter how volatile cryptocurrencies seem, and adoption is advancing far faster than regulations can catch up, Coinbase is backstopped by institutional demand and regulatory necessity across the developed world.

If you’re not familiar with the company, don’t worry. Check my essay on what the company is attempting to build -

If you’re new to my research or want a quick sense of how I approach investing, you can have a look at my investing process.

TLDR:

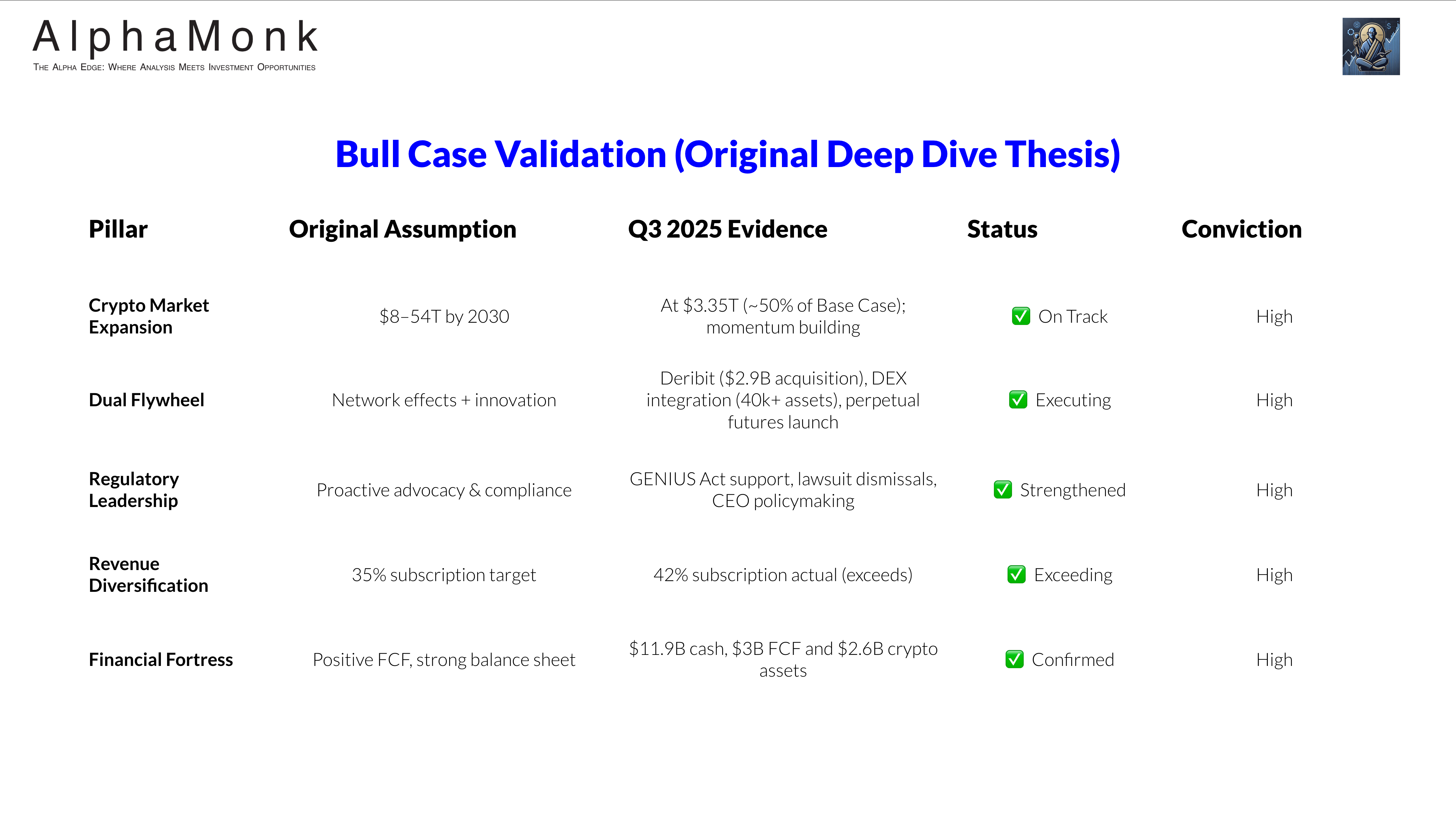

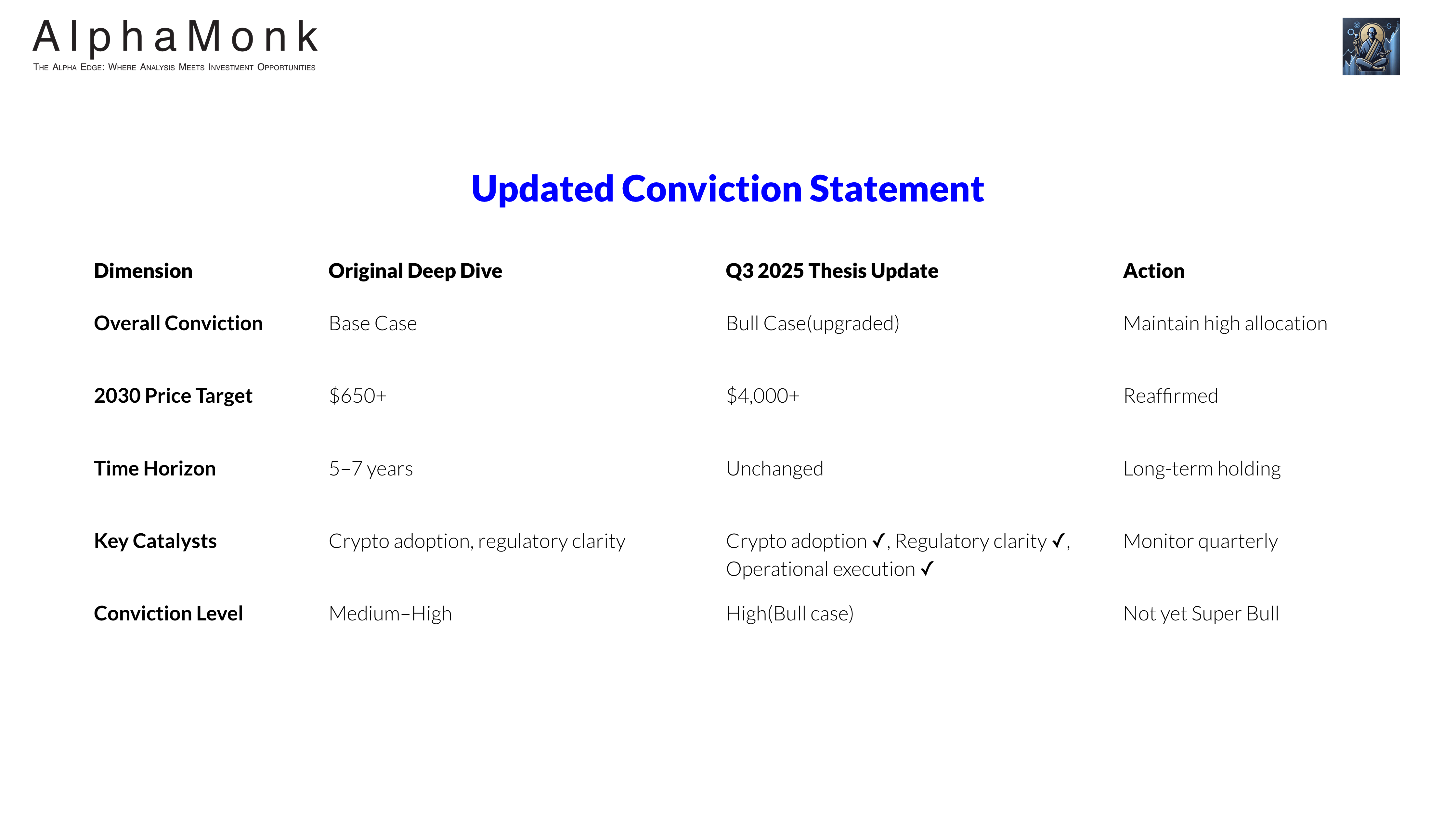

Conviction reinforced: Coinbase’s Q3 2025 performance strongly validates its Bull Case thesis, driven by strategic diversification, institutional adoption, and robust execution on its “Everything Exchange” vision.

Coinbase’s Q3 results seem to be 65-75% beta-driven on a trading basis, but the technical charts hide 25-35% of alpha already in the valuation due to operational execution.

Revenue Diversification: Coinbase achieved $5.2B in net revenue in the first three quarters of FY2025. Subscription and services revenue made up 40% of the revenue thus surpassing my long-term target of 25–35%, indicating accelerated progress towards stable, recurring income.

Profitability & Cash Flow: Net income surged 477% year-over-year to $432 million. The business generated $1.8B in free cash flow for the first nine months of 2025 and maintains a strong balance sheet with $11.9 billion in cash and cash equivalents.

Institutional Dominance: Assets Under Custody (AUC) hit an all-time high of $516B, including $300B in institutional custody. Coinbase is the primary custodian for over 80% of US Bitcoin and Ethereum ETF assets. The company is positioned as the partner of choice for financial institutions, such as Citi, as regulatory clarity accelerates.

“Everything Exchange” Strategy: Key strategic moves include the $2.9 billion acquisition of Deribit (the leading crypto options exchange), the launch of US Perpetual Futures (addressing 80% of global crypto trading volume), and the continued scaling of the Base Layer 2 network.

Investment Conclusion:

Outperformance: Coinbase’s stock gain (105% increase since my May 2025 recommendation) has significantly outperformed the growth of the underlying crypto market cap (53% increase), suggesting the market is valuing the company for operational execution (alpha), not just crypto market correlation (beta).

Valuation: The stock price, currently consolidating around $290+, has the potential to rise to over $400 per share within the next 2–3 years. My thesis maintains the possibility of the stock exceeding $500 per share by late 2027.

Verdict: As a long-term investor with a 5-7 year horizon I am holding the stock and will keep adding tactically any dip below $300, acknowledging risks like crypto market volatility, Binance competition, fee compression, and regulatory uncertainty in international markets.

Now to the article.

Read my full disclaimer.

I own COIN 0.00%↑

COIN 0.00%↑ at $310+: Conviction Meets Consolidation

When I recommended Coinbase at $140-$150 in April and May 2025, my thesis rested on a rather straightforward premise: the market was mis-pricing the plumbing that would underpin the next cycle of crypto adoption.

The stock had been battered by regulatory uncertainty, institutional indifference, and the lingering hangover of the 2022-2023 crypto winter. It was cheap in a way that made sense only if you believed the fundamentals would recover. Fast forward seven months, having watched the share price more than double to $307 and at one point touched $440 in mid-July (when your’s truly did book some profits), I ask whether my initial thesis has run its course or merely begun.

The chart reveals an intriguing story. From the May 2025 recommendation price of $145, Coinbase’s value has increased by about 112%, a gain that seemed overly optimistic at the time. However, the current technical picture suggests neither extreme optimism nor pessimism. The stock is above all three primary moving averages: the 20-week, 50-week, and 200-week averages are at $341.53, $284.15, and $165.50 respectively, indicating a healthy intermediate uptrend with genuine structural support.

Interestingly, the consolidation pattern around $320-$340 is noteworthy. The Relative Strength Index, hovering near 50.77, suggests no signs of exhaustion, indicating neutral territory rather than an overbought signal. Volume compression suggests institutional investors are absorbing supply, which is a bullish sign. The MACD remains positive but is flattening, neither suggesting runaway momentum nor imminent reversal.

The original thesis was based on three critical claims: one - that revenue diversification would exceed expectations, two - that custody assets would consolidate Coinbase’s institutional moat, and three - that the regulatory environment would become more favourable. The Q3 results delivered on each front. Subscription revenue now accounts for 42% of total net revenue, surpassing the 25-35% target. Assets Under Custody reached an all-time high of $300 billion, capturing 12.9% of the $4.0 trillion crypto market capitalisation. While the regulatory landscape is not ideal, it has become more constructive, particularly following progress in stablecoin legislation.

The question is whether the chart’s consolidation indicates the end of a speculative rally or a necessary pause before the next upward leg. A decisive break above the 20-week moving average ($340) would suggest continuation towards $360-$400. Conversely, a retreat to the 50-week average ($284-$290) would test the sustainability of the uptrend or the inevitability of a mean reversion.

From a conviction standpoint, the consolidation is healthy. Investors who bought at $140-$150 now have a choice: lock in gains, average up on dips, or hold for the $500+ thesis that still seems achievable by late 2027. The technical setup suggests patience will be rewarded over the next 12-24 months. The bulls haven’t lost the initiative, and the bears haven’t regained credibility. We have to wait for the next catalyst to decide the outcome.

Is the ‘Everything Exchange’ that catalyst?

Coinbase’s Q3 strategic initiatives advanced its ‘Everything Exchange’ vision—a unified platform for trading various asset classes, including spot crypto, derivatives, prediction markets, equities, and tokenised real-world assets launched in Q2 2025.

The progress made to date includes:

Deribit Acquisition (Completed August 2025): Coinbase’s $2.9 billion acquisition of Deribit, the world’s leading crypto options exchange with over 75% global market share, marks its most significant M&A deal. Deribit contributed $52 million in Q3 revenue, and combined, they have a notional derivatives trading volume exceeding $840 billion. To focus on profitability, Coinbase is scaling back rebates and incentives in the derivatives business. Cross-margining between US futures and spot, introduced in Q3, offers a 2x capital efficiency advantage. The integration roadmap aims to unify spot, perpetual futures, and options under a single institutional interface, enhancing cross-selling and client stickiness. Read my Deribit acquisition essay here:

US Perpetual Futures Launch: Coinbase launched CFTC-regulated, 24/7 crypto perpetual futures for Bitcoin, Ethereum, Solana, and XRP in the US, offering up to 10x intraday leverage. This product led the US crypto derivatives market in Q3, addressing the 80% of global crypto trading volume that occurs in derivatives markets, historically dominated by offshore exchanges.

DEX Integration: Integrating decentralised exchange functionality into the Coinbase consumer app increased tradable assets from about 300 to over 40,000, covering about 90% of the total crypto asset market capitalisation. This strategy exposes early-stage tokens to price discovery, with successful assets moving to Coinbase’s centralised exchange for deeper liquidity and tighter spreads. Early success is shown by increased Advanced trading volumes and higher share-of-wallet from retail customers.

Base Layer 2 Momentum: Base, Coinbase’s Ethereum Layer 2 network, continues scaling with sub-second, sub-cent transactions. The ecosystem now has over 5 million tokens and 16 local-currency stablecoins, with ‘Flashblocks’ technology delivering 200-millisecond block times. Base revenue growth in Q3 was driven by higher average Ethereum prices and transaction volumes, but average revenue per transaction declined as the network prioritises scalability. The Base app entered beta, offering trading, mini-apps, social features, and USDC payments via universal ‘Base Account’ identity. Learn more about Base in my essay on the topic:

USDC Ecosystem Expansion: USDC market capitalisation hit an all-time high of $74 billion, with Coinbase customers contributing the largest share of Q3’s $12 billion growth. This highlights Coinbase’s role as the preferred USDC distribution channel. Average on-platform USDC balances of $15 billion (up 9% quarter-over-quarter) generate recurring stablecoin revenue through Circle’s revenue-sharing arrangement. Off-platform USDC balances reached $53 billion (up 12% quarter-over-quarter), but the shift towards on-platform holdings is compressing the off-platform yield due to Circle’s focus on growing its own on-platform partnerships. Payments infrastructure expanded with 1,000 businesses onboarding to Coinbase’s B2B payment APIs and UI, targeting the $40 trillion cross-border payments market (75% of which is B2B).

Institutional Custody Dominance: Assets under custody hit a record high of $300 billion, fuelled by strong inflows from native units in ETFs (Coinbase is the primary custodian for over 80% of US Bitcoin and Ethereum ETF assets) and corporate purchases. Coinbase’s partnership with Grayscale to launch the first US staking ETFs in October 2025 further solidified its custodial position.

Verdict: Thesis reinforced with high conviction.

Financial Performance: Diversification Delivers Resilience

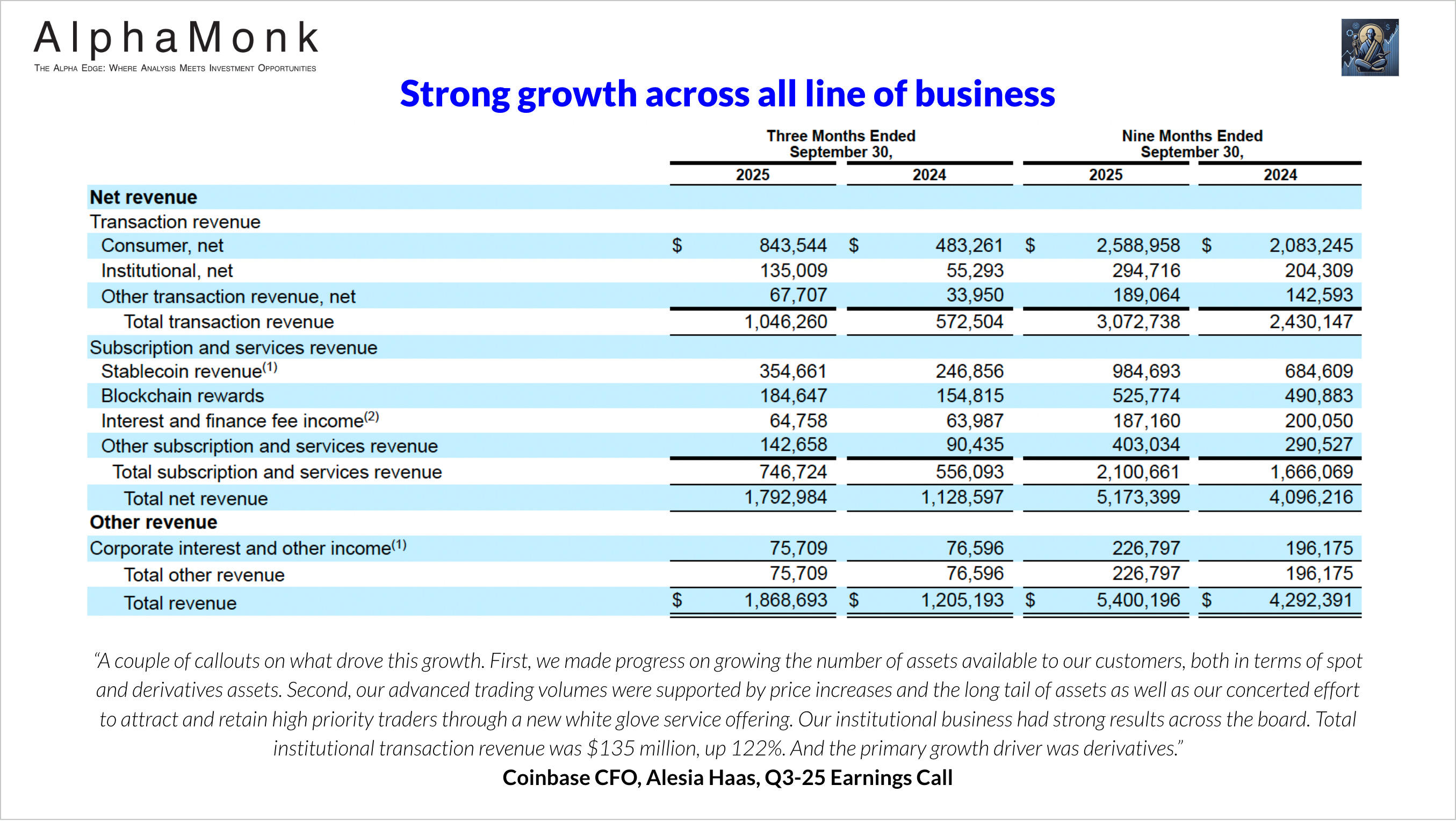

Coinbase’s Q3 2025 financial results mark a turning point in the company’s evolution from a transaction-fee-based exchange to a diversified financial services platform. Total revenue of $1.87 billion was split into $1.05 billion in transaction revenue (58% of net revenue) and $747 million in subscription and services revenue (42%), a significant shift from the 51%/49% split in Q3 2024. This 42% subscription weighting surpasses my Deep Dive’s 2025 target of 25-35%, indicating accelerated progress towards revenue stability.

$1.05 billion in transaction revenue (58% of net revenue): Transaction revenue grew 83% year-over-year to $1.05 billion, driven by strong trading activity and the Deribit acquisition. Consumer revenue increased 30% quarter-over-quarter to $844 million, fuelled by a 37% growth in consumer trading volume.

$747 million in subscription and services revenue (42%): Subscription and services revenue was $747 million, with stablecoin revenue growing 7% to $355 million. Blockchain rewards revenue rose 28% to $185 million, while interest and finance fee income grew 9% to $65 million.

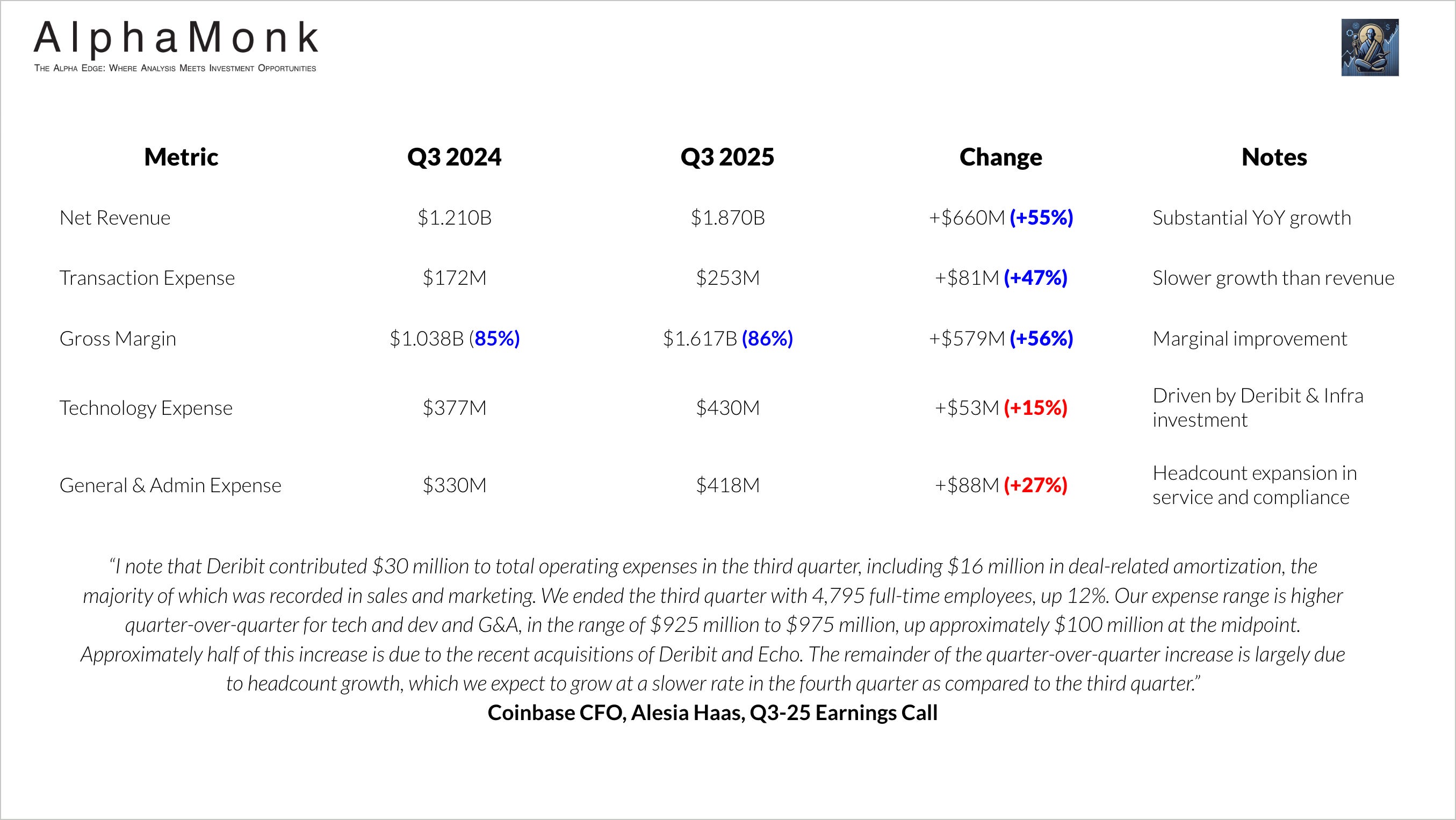

Gross margin expanded marginally to approximately 86% (calculated as net revenue less transaction expense), up from 85% in Q3 2024, evidencing operating leverage. Transaction expenses increased 47% to $253 million, driven by higher blockchain rewards fees (reflecting elevated crypto asset prices) and increased customer trading activity, but grew more slowly than revenue. Technology and development expenses rose 11% quarter-over-quarter to $431 million, incorporating Deribit personnel and infrastructure investments, whilst general and administrative expenses increased 18% to $418 million, primarily due to headcount expansion in customer service and global compliance.

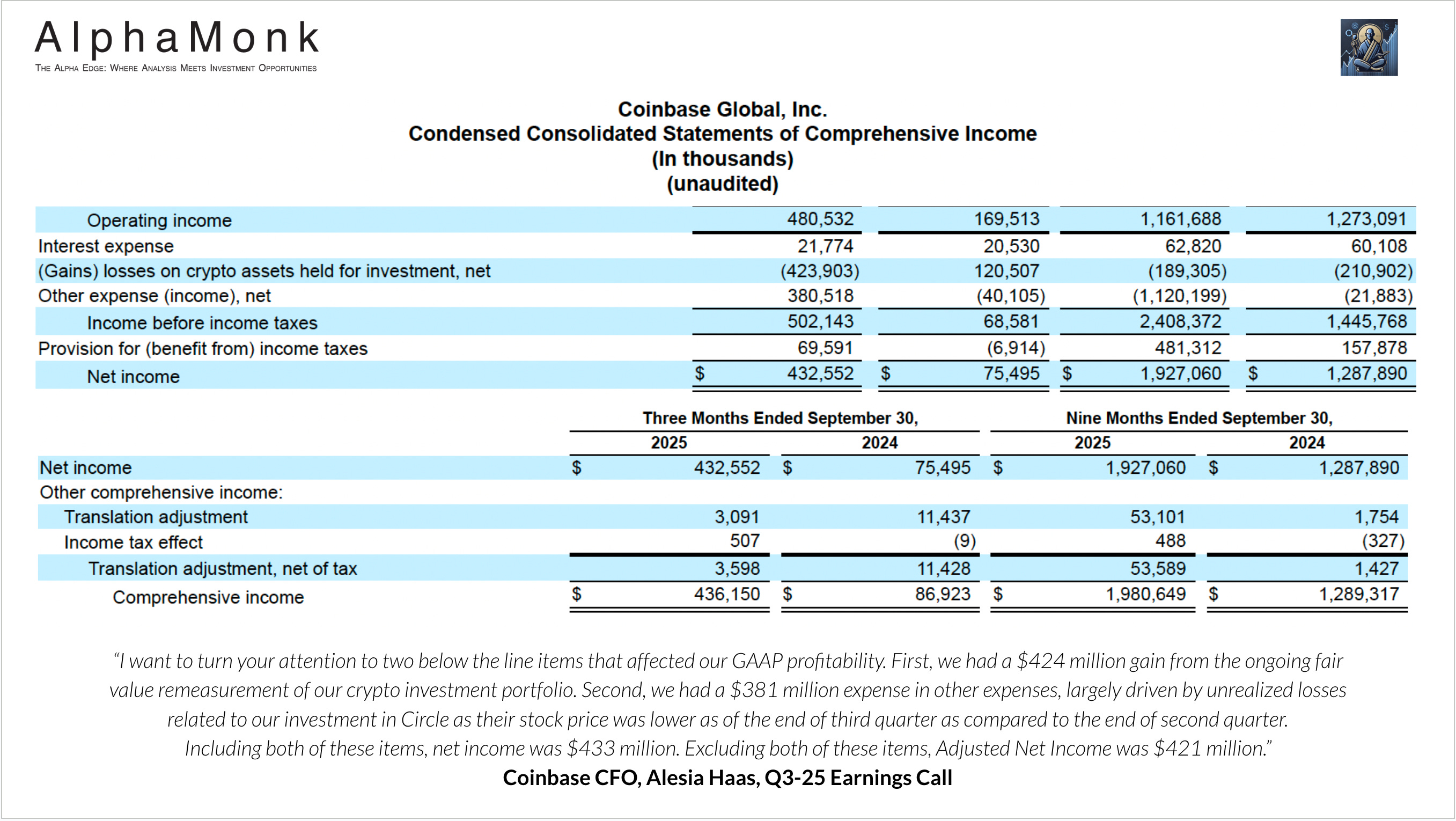

Net income rose to $432 million, a 477% increase from Q3 2024’s $75 million. However, this includes $424 million in gains from crypto investments and $381 million in losses from strategic investments (mainly Circle). Adjusted Net Income, excluding these non-operating items, was $421 million, and Adjusted EBITDA was $801 million, a 43% margin on net revenue, showing strong profitability.

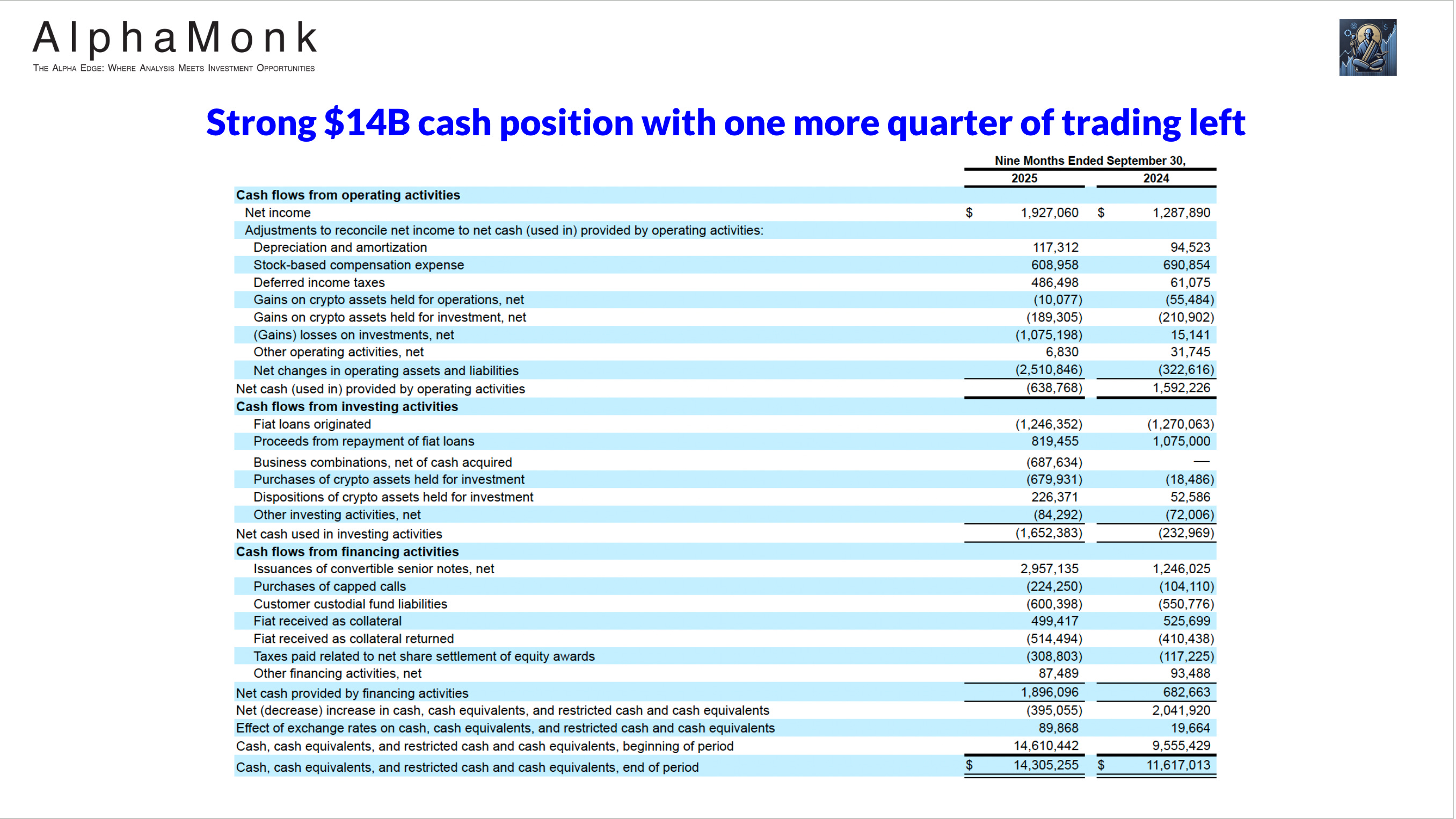

Free cash flow generation remains strong at $1.8B generated in FY2025, though specific Q3 figures are embedded within the nine-month 2025 results. The company ended the quarter with $11.9 billion in USD resources (up 28% from December 2024), comprising $8.7 billion in cash and equivalents, $3.2 billion in USDC, and $7.0 billion in money market funds. Additionally, Coinbase holds $2.6 billion in crypto assets for investment (up 68% from year-end 2024), bringing total available resources to $15.5 billion when including crypto holdings.

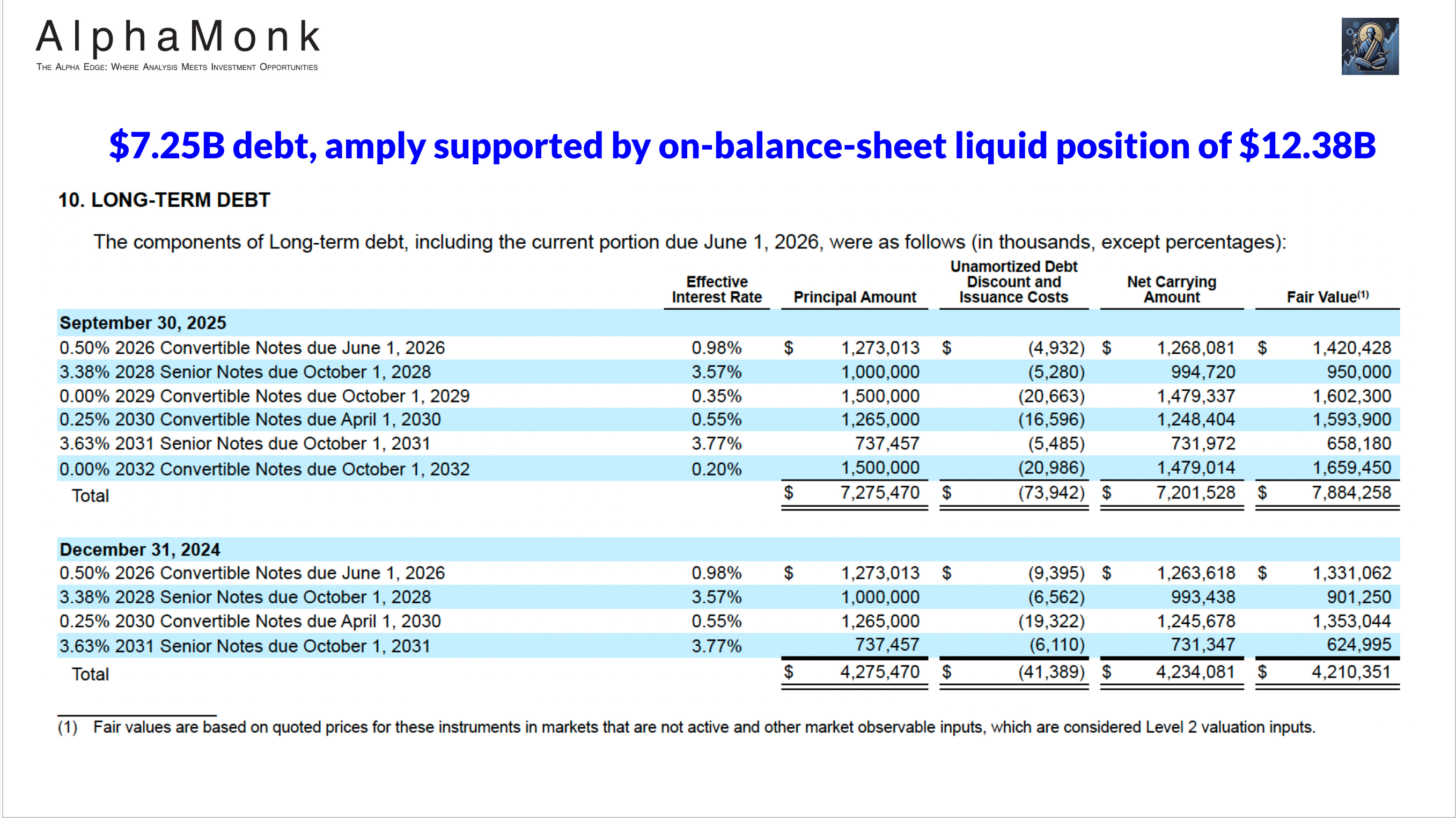

Coinbase’s long-term debt stood at $5.93 billion as of September 30, 2025, with an additional $1.27 billion in current portion of long-term debt, totalling $7.2 billion. However, liquidity supports these liabilities: cash and cash equivalents were $8.68 billion, and USDC held $3.70 billion, totalling $12.38 billion on the balance sheet. Even excluding USDC, cash alone exceeds all outstanding debt.

The business generated $1.8B in free cash flow for the nine months ended September 2025, despite acquisition outflows and working capital investments. Annualising this figure suggests robust cash generation power, which, combined with the current treasury, could retire the entire debt without growth investments.

In summary, current debt maturities are covered multiple times over by cash, and ongoing free cash flow generation makes the debt position exceptionally conservative for a large and cyclical business.

Outperforming expectations on core metrics in comparison to my investment thesis

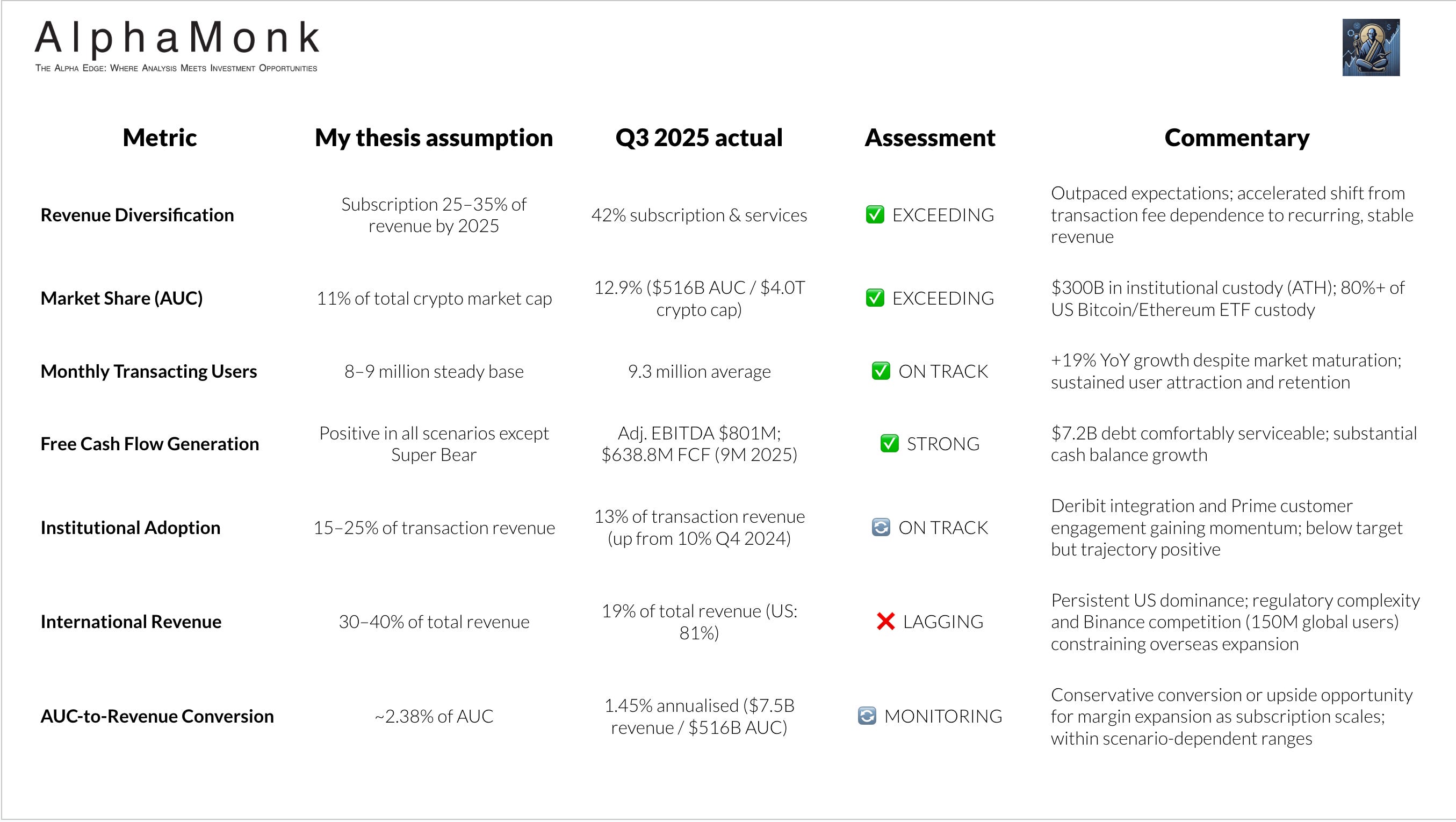

My first Deep Dive, published in May 2025, provided a comprehensive framework for evaluating Coinbase’s long-term potential. I projected scenarios from a ‘Super Bear’ (crypto market cap declining to $340 billion by 2030) to a ‘Super Bull’ ($54 trillion by 2030). My Base Case assumed a crypto market capitalisation of around $8 trillion by 2030, with Coinbase holding 12% of Assets Under Custody and generating about 2.38% of AUC as revenue. Q3 2025 results confirm and exceed the Deep Dive’s assumptions in several ways.

Revenue Diversification: Coinbase surpassed the Deep Dive’s target, with subscription revenue reaching 42% in Q3 2025, exceeding the projected 25-35%.

Market Share: Coinbase achieved a 12.9% market share in Assets Under Custody, exceeding the Deep Dive’s 11% assumption.

Assets Under Custody: Coinbase reached $516 billion in Assets Under Custody, with $300 billion in institutional custody, representing an all-time high.

User Growth: Monthly transacting users reached 9.3 million in Q3 2025, reflecting a 19% year-over-year growth.

Financial Performance: Coinbase generated $801 million in Adjusted EBITDA in Q3 2025, confirming its ability to service its debt and sustain positive free cash flow.

Institutional Adoption: Institutional transaction revenue increased to 13% of total transaction revenue, indicating positive growth despite falling short of the target range.

Revenue Generation: Coinbase’s Q3 annualised revenue run rate is $7.5 billion against $516 billion AUC, yielding a 1.45% ratio.

Valuation Framework: The Deep Dive’s valuation framework anticipated Coinbase generating revenue at approximately 2.38% of Assets Under Custody.

Potential Margin Expansion: The current revenue-to-AUC ratio suggests either conservative AUC-to-revenue conversion or potential for margin expansion as subscription services scale.

Does the share price still reflect the overall value of the crypto market?

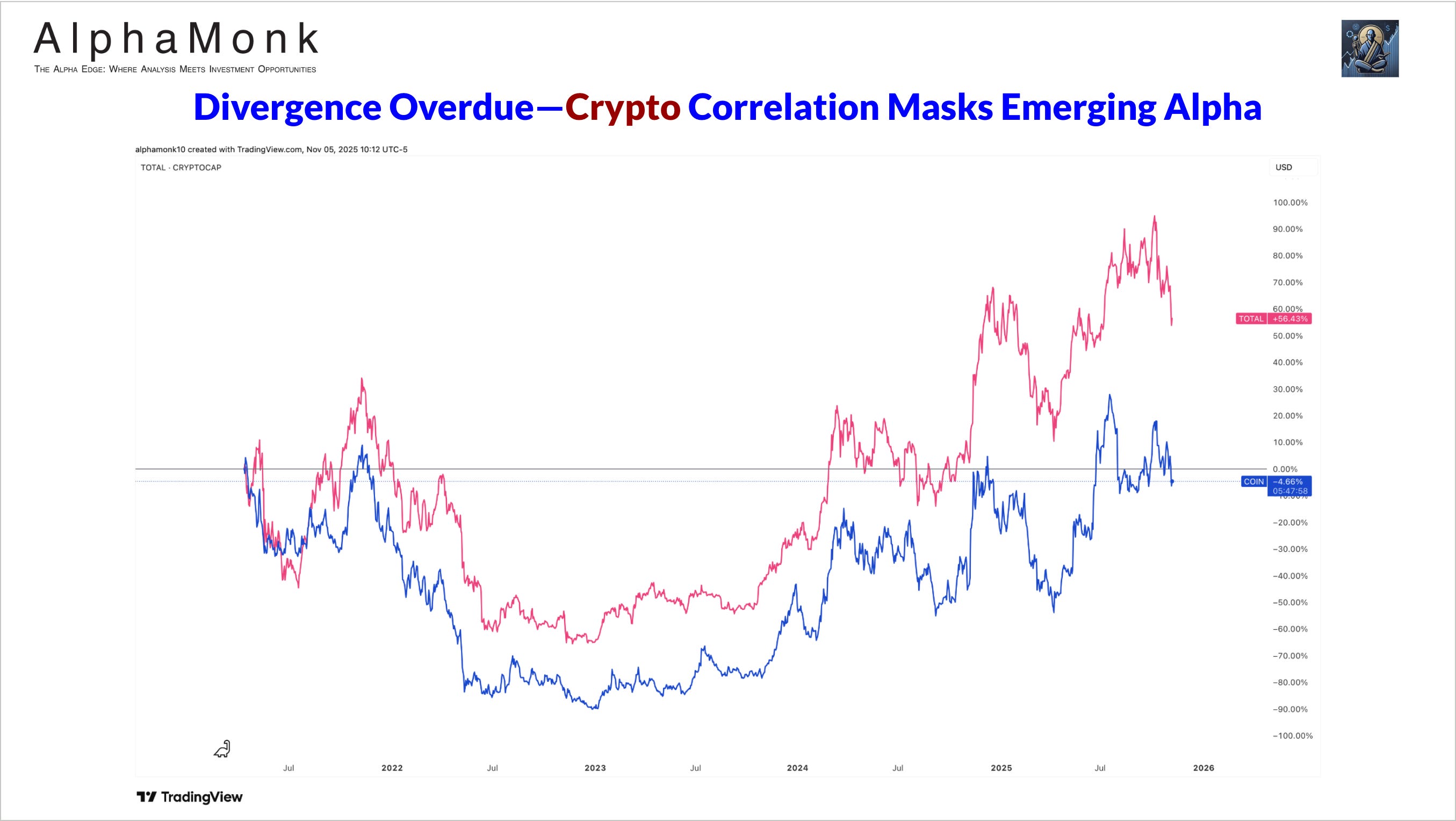

The chart shows a close correlation between Coinbase’s (blue line) and total cryptocurrency market capitalisation (magenta line) since 2021, especially through 2024 and early 2025. The pattern suggests a strong correlation - when crypto goes up Coinbase follows suit and vice versa.

But, I think a divergence set up is forming suggesting Coinbase’s valuation is influenced by both market sentiment and company-specific factors. The market is valuing COIN 0.00%↑ for not only for its crypto balance sheet but also as an operating business. Why do I think that might be the case? Let me explain.

Q3 performance was no doubt boosted by favourable crypto market conditions. Total crypto market capitalisation grew by $564B (+16.4%) to $4.0 trillion, marking the sector’s third consecutive quarterly gain and its second successive quarter of significant capital accumulation. However during the same period Coinbase shed $3.5B (-3.5%). So in a sense on a quarterly basis the correlation was not so pronounced. However if I rewind back to my entry price of $140–$150 during April/May 2025, Coinbase’s value has increased to $307 a 105% increase, while the total crypto market cap has grown from $2.6 trillion to $4.0 trillion, a 53% increase. Coinbase’s 105% gain has outperformed the underlying crypto market by 52 percentage points.

This in my opinion is a sign of maturity. As crypto markets mature and Coinbase captures incremental market share through product innovation and operational excellence, its valuation should decouple positively from pure crypto beta.

To conclude, the chart’s apparent ‘tight correlation’ might be misleading. What seems like correlation is actually early-stage outperformance being absorbed by a rising market. The key moment will be when the total crypto market cap stops growing or starts to fall (a ‘Super Bear’ or consolidation phase), but Coinbase’s value is still supported by 42% subscription revenue, $300 billion in institutional custody, and positive free cash flow. This difference between correlation breaking down during a sideways or declining crypto market will reveal whether Coinbase’s premium is justified or just a gamble. The real thesis acceleration happens when macro crypto conditions normalise and this correlation breaks. My monitoring framework should anticipate this divergence, not discount it.

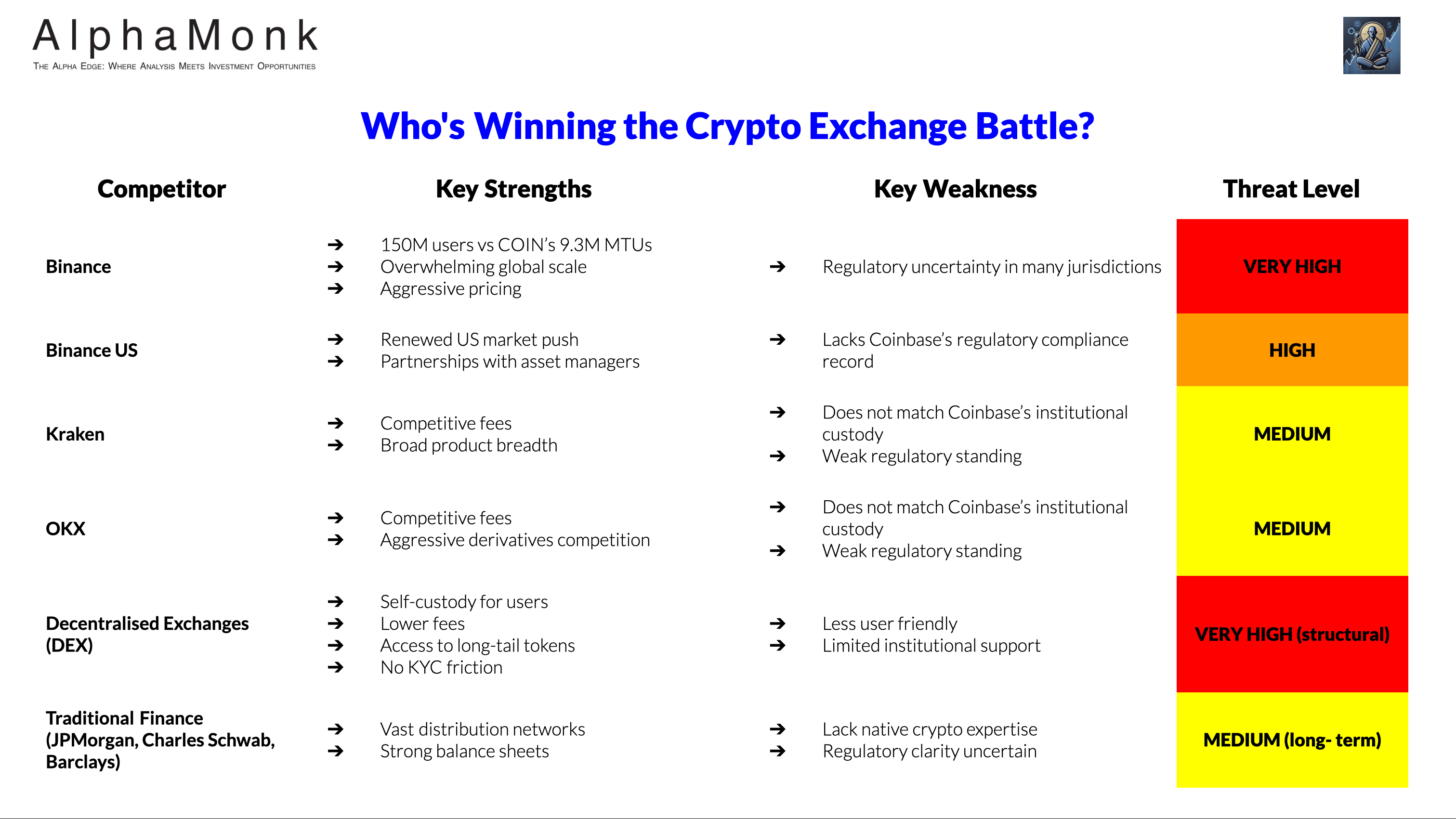

Competitive Assessment: Regulatory Moat Meets Scale Threat

Verdict: Coinbase’s competitive position has strengthened in Q3, principally through Deribit’s acquisition and perpetual futures launch, which address the historically weak derivatives offering. Regulatory moat and institutional custody dominance remain durable advantages. However, Binance’s global scale and aggressive pricing pose persistent share threats, whilst DEX integration may prove a double-edged sword if users migrate to fully decentralised alternatives.

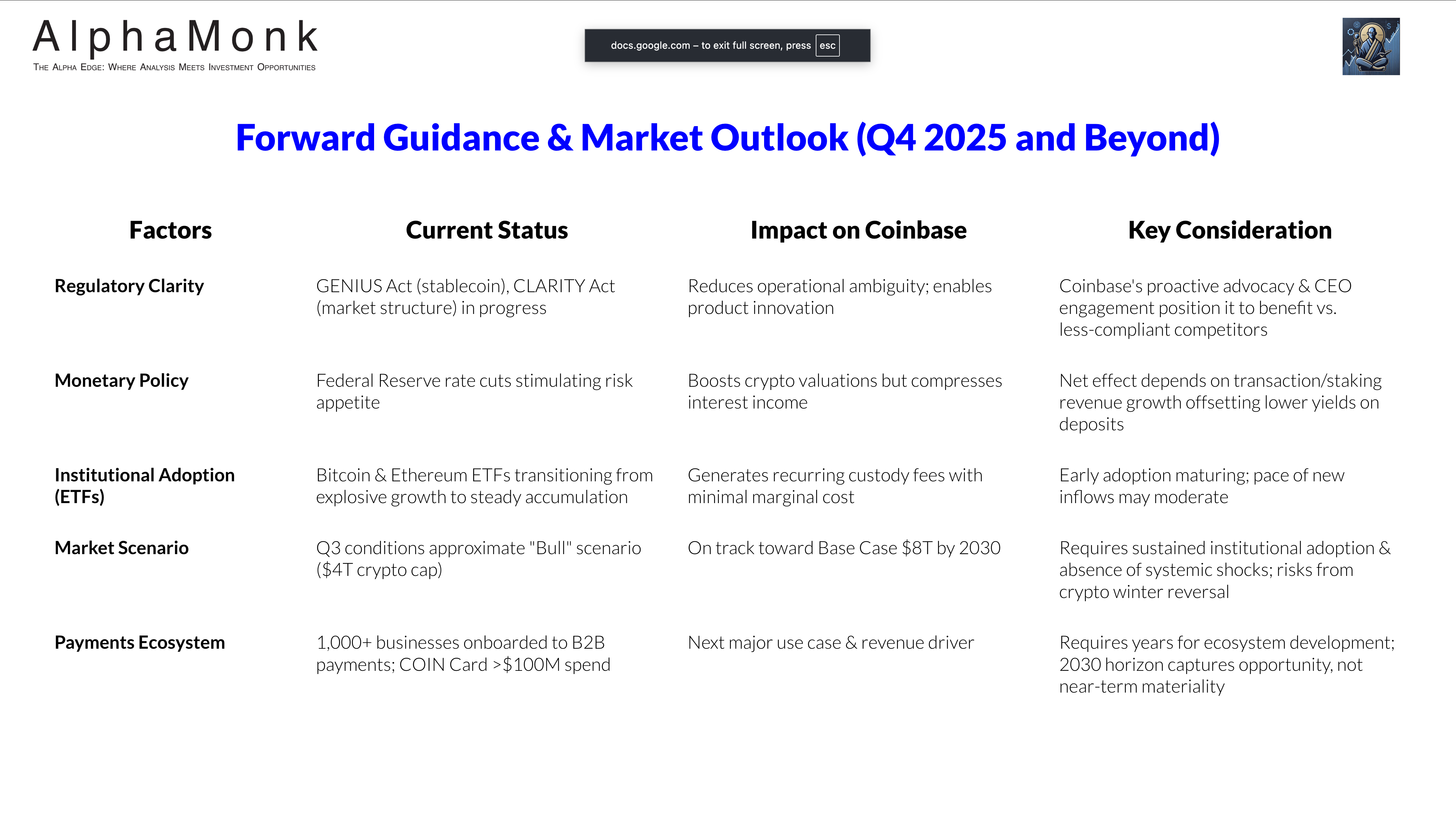

Navigating Crosscurrents: Forward Guidance and Market Outlook

Alesia Haas and Brian Armstrong provided Q4 2025 guidance indicating continued growth, but with normalising trends.

October transaction revenue is estimated to be around $385 million, which annualises to $1.54 billion quarterly. This suggests a moderation from the $1.05 billion in Q3, although October typically has lower volumes than summer.

Subscription and services revenue is projected to be between $710 million and $790 million in Q4. This reflects USDC market cap growth and Coinbase One subscriber expansion, but is offset by anticipated Federal Reserve interest rate cuts compressing interest income.

Operating expenses are expected to rise significantly, with technology and development plus general and administrative expenses projected to be between $925 million and $975 million. This increase is due to full-quarter Deribit and Echo integration and headcount growth.

Headcount growth will slow in Q4 compared to Q3, and that sequential operating expense growth in early 2026 will slow as the company absorbs 2025’s talent additions and focuses on execution rather than expansion.

Sales and marketing expenses are projected to be between $215 million and $315 million, with the range driven by performance marketing opportunities and USDC rewards tied to on-platform balances.

Beyond Q4, several macroeconomic and regulatory factors shape the outlook:

Coinbase’s proactive advocacy and diversified revenue base position it to benefit from regulatory clarity and potential crypto market growth. However, fee compression, regulatory challenges, and market volatility pose risks to its growth trajectory.

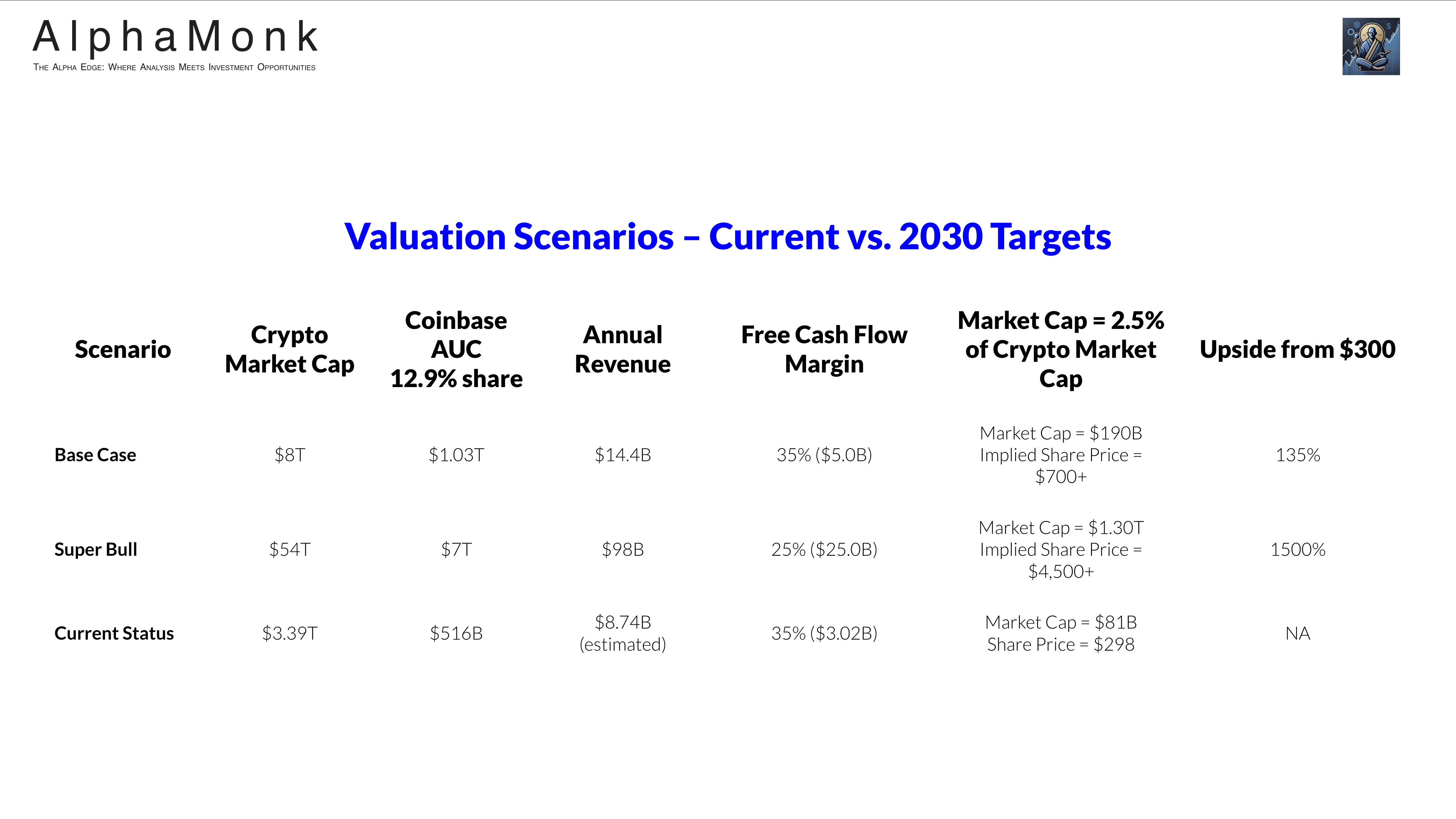

Valuation and Thesis Reassessment: Conviction Reinforced

Coinbase’s Q3 2025 performance, with a 12.9% market share and $1.87 billion revenue, surpasses my Base Case assumptions from the original Deep Dive. This suggests my initial projections may have been conservative, particularly regarding market share and revenue growth.

Updated Valuation Framework:

Coinbase’s current fair value is approximately $196 per share, aligning with May 2025 levels. However, the investment thesis is based on 2030 potential, with a base case scenario projecting a $303 per share valuation and a Super Bull scenario suggesting a valuation exceeding $450 per share.

Thesis Reassessment:

Q3 results validate the bull case for Coinbase, highlighting crypto market expansion, the dual flywheel of network effects and innovation, regulatory leadership, revenue diversification, and a strong financial position.

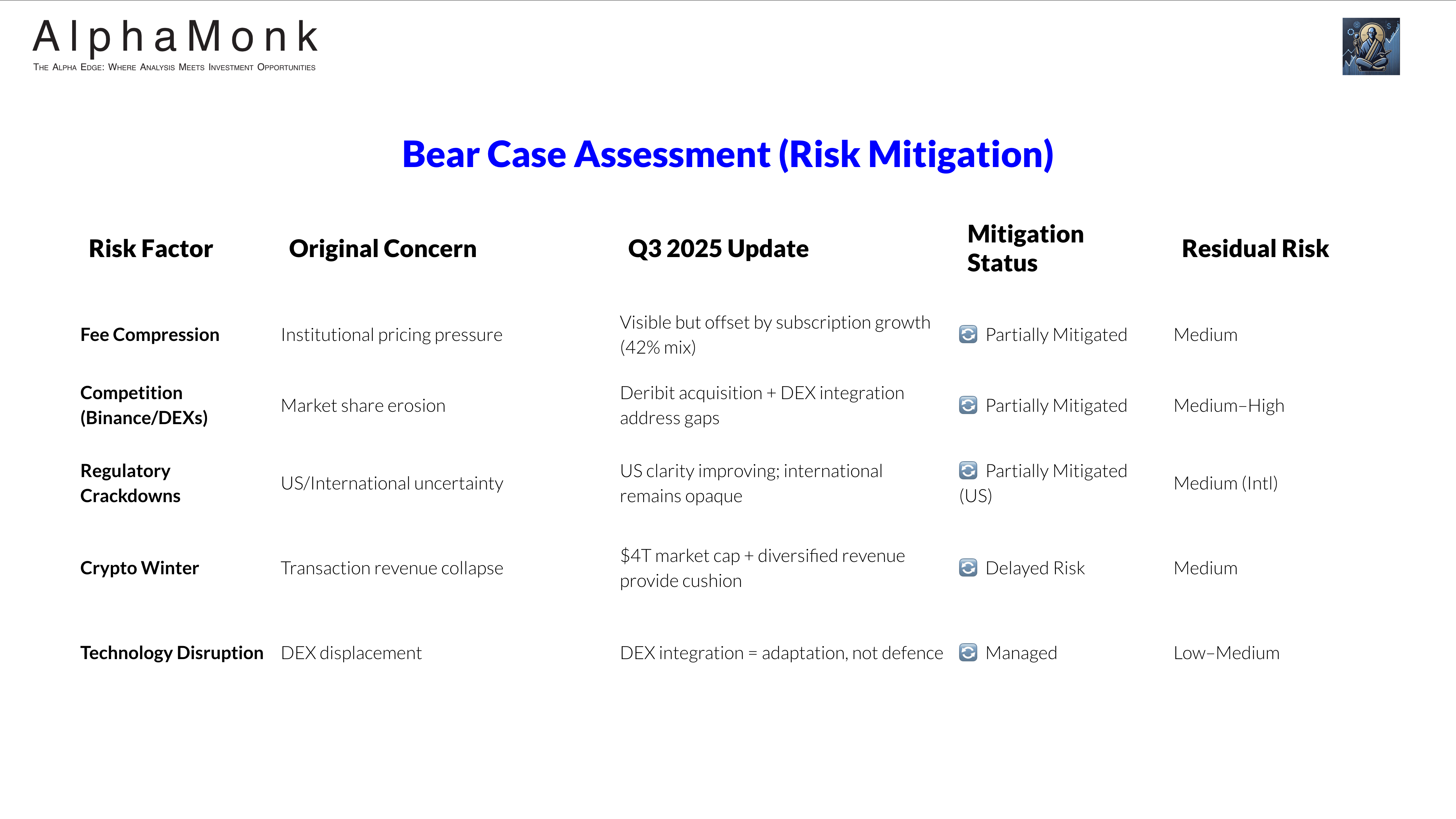

Q3 developments partially mitigate concerns about fee compression, competition, regulatory crackdowns, a prolonged crypto winter, and technology disruption. Institutional pricing pressure is offset by subscription growth, while Binance remains a formidable competitor.

Updated Conviction: Q3 execution warrants upgrading conviction towards Bull Case, though not yet Super Bull. The 2030 target of $300-$450 per share remains credible and achievable.

Conclusion: Asymmetric Opportunity with Execution Risk

Q3 2025 Performance: Coinbase’s Q3 2025 results exceeded expectations, demonstrating strong execution on strategic goals like revenue diversification and product expansion.

Bullish Outlook: Positive factors include crypto market growth, regulatory clarity, and Coinbase’s “Everything Exchange” strategy, potentially driving the stock price to $700+ by 2030.

Bearish Concerns: Binance’s market dominance, fee compression, limited international expansion, and potential market downturns pose risks.

Final Assessment:

My Investment Approach: High Conviction Buy at prices lower than $300 with a 5-7 year horizon and I accept cryptocurrency market volatility.

Key Performance Indicators: Monitor quarterly subscription revenue growth, international revenue mix, institutional transaction revenue, free cash flow, and AUC market share.

Thesis Invalidation Triggers: Sustained negative free cash flow for three consecutive quarters, loss of major banking/custodial relationships, or Bitcoin declining below $50,000 for extended periods.